What IS going on with mobile payments? Physical wallets were supposed to be obsolete by now. We were supposed to be paying for everything with a nonchalant swipe of our smartphones.

And yet here we are in 2014, pulling the same tired old plastic debit cards out of the same tatty leather pouches. This isn’t the future we envisaged back in 2010.

We’re being overly dramatic, of course. But the question is a valid one. Are we really any closer to that wallet-free future?

Yes. In fact, some of the major changes necessary to kickstart the widespread adoption of mobile payments are right around the corner.

Allow us to explain.

Mobile payments: here already

Mobile payments are already here. They’re just not very widespread, and they’re not particularly good.

Google tried its luck three years ago with Google Wallet, a payment system that worked with NFC technology incorporated into Android phones of the time. The company has ploughed hundreds of millions into it and struck deals with several major financial institutions, but it still hasn’t taken off.

Indeed, Google Wallet NFC payments still aren’t available outside of the US. It all just seems to have stalled for the big G.

Samsung has had a somewhat half-hearted stab at mobile payments by adding support for Visa’s own payWave app to its NFC-equipped smartphones. It’s not a stand-alone integrated system, though.

Nokia was the first smartphone manufacturer to launch an NFC-equipped phone some eight years ago, but it’s still been unable to crack the mobile payment conundrum. Rather, it seems to have focused on NFC’s facility to make Bluetooth pairing quick and easy with things like speaker docks and headsets.

Why haven’t mobile payments taken off yet?

There are a number of reasons (and excuses) that have been offered up as to the failure of mobile payments to really take off.

The main one seems to be the expense involved for retailers. Put simply, a large proportion of shops do not have the NFC-scanning equipment in place to accept such mobile payments – and show little will to do so. With no immediate benefit, particularly for smaller retailers, it’s easy to see why this has been the case.

This is particularly so in the American market, which poses its own distinct problem. It’s the home of so many mobile payment innovators, and is invariably the first major market that most technical innovations of this kind must tackle if they’re to take off.

Yet America has been extremely resistant to new, more advanced payment systems. Most places you go in the US, you still have to sign for credit card purchases.

Another thing that’s hampered the take-off of mobile payments in the US market is the power and influence of the mobile network operators. In addition to NFC technology, network support is needed to facilitate secure mobile payments.

American networks – or ‘carriers,’ as they’re called natively – combined to pretty much scupper Google (one of few companies in a position to get things rolling) and it’s ambitions in the space. These operators opted not to support Google Wallet, instead choosing to adopt their own mobile payment system called ISIS.

Of course, all of this squabbling over multiple standards is in itself a factor in the lack of mobile payment progress.

Finally, there are concerns over the security of mobile payment systems. Consumers will need solid reassurance that their mobile phones and network connections are secure enough to be trusted with their bank details – and with numerous and ongoing tales of remote hacking and malware (particularly on Android), that confidence just hasn’t come about.

Why mobile payments are about to take off

For one thing: Apple. The tech world has been anticipating Apple’s adoption of NFC and launch of its own mobile payment system for several years now. Many feel that Apple’s non-participation alone has been enough to stall the widespread adoption of mobile payments.

While we wouldn’t go quite that far, there’s little doubt that Apple’s non-participation has been a major factor. Apple, with its hugely popular iPhone range, has an uncommonly strong say on such standards.

You might think that if simple market saturation was such a factor, then Google and Samsung’s efforts would have seen greater success. But it’s not simply down to the sheer number of iPhone and iOS users out there. Apple has a singularly strong and secure software ecosystem, and customers who are willing to spend good money through as well as on its devices.

It’s been estimated that Apple has some 800 million credit cards stored on its system already – that’s more than twice what Amazon and Paypal have combined. If it decides to implement an intuitive mobile payment system of its own, it would be a relatively small matter to switch a vast number of those users onto it.

And all reports suggest that Apple is indeed implementing such a system. In fact, the iPhone 6 will almost certainly be announced on September 9 with NFC support and Apple’s own mobile payment system onboard. The company has reportedly reached agreements with Visa, Mastercard, and American Express to support such a system.

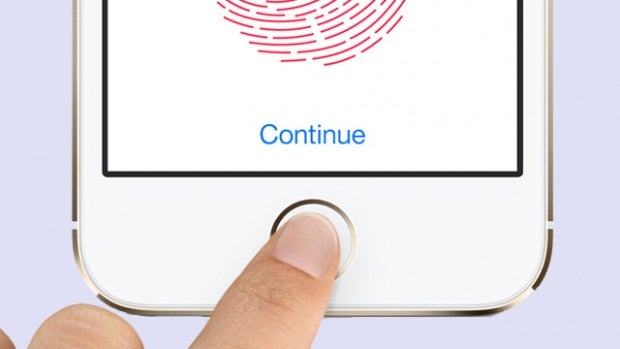

What’s more, with Apple’s proven Touch ID system on board, users will be able to use their own fingerprints to authorise payments – something that will be quick, easy, and most importantly secure.

The only potential hitch here is the carriers, but Apple has shown in the past that it’s uniquely capable of bulldozing its way through such petty roadblocks.

Aside from Apple’s involvement, the situation with US retailers is also looking up. Recent legislation has meant that American shops are having to upgrade their payment-handling equipment to accept the kind of chip and pin cards we in Europe have had for years.

Many of the latest payment systems of this kind will have NFC systems built in, meaning a significant portion of America is soon going to be mobile payment-ready. Much of Europe is already prepared, or will be soon.

Of course, the one remaining major factor in all of this is the consumers. Are we all ready for mobile payments? Do we even want to ditch our wallets and hand another part of our lives over to our smartphones? That’s the one lingering question that even Apple can’t be sure of the answer to.

Next, check out all the latest iPhone 6 rumours and news

Editorial independence

Editorial independence means being able to give an unbiased verdict about a product or company, with the avoidance of conflicts of interest. To ensure this is possible, every member of the editorial staff follows a clear code of conduct.

Professional conduct

We also expect our journalists to follow clear ethical standards in their work. Our staff members must strive for honesty and accuracy in everything they do. We follow the IPSO Editors’ code of practice to underpin these standards.

Editorial independence

Editorial independence means being able to give an unbiased verdict about a product or company, with the avoidance of conflicts of interest. To ensure this is possible, every member of the editorial staff follows a clear code of conduct.

Professional conduct

We also expect our journalists to follow clear ethical standards in their work. Our staff members must strive for honesty and accuracy in everything they do. We follow the IPSO Editors’ code of practice to underpin these standards.